Feature/Technology

ONE PLATFORM, MANY BANKS

Treasury can simplify the

management of its trade-related activities using a web-based, multi-bank

platform

By Jacob

Katsman

Over the last seven years, trade banks have developed web-based front-end systems to capture information from their corporate clients, such as an import letter-of-credit application, and deliver the information from a bank’s back-office system to clients, such as advice of payment details. At best, such front-end systems are fully integrated into the bank’s back office. Information flows seamlessly from the corporate customer to the bank without manual intervention from the bank’s staff. At worst, some systems just capture the information from the corporate via a web form; the bank’s processing staff then has to cut and paste this information into the bank’s system or systems.

With such solutions, banks hoped to replace telex,

fax, phone, and courier communication. For corporate customers that dealt only

with one bank, a one-to-one front end works fine. But for corporate customers with multiple banking relationships,

dealing with different bank systems is inefficient. Staff need different

training in each system and different user names and passwords. To view the

organization’s overall outstanding position across all banks in terms of

liability, credit availability, risk exposure and bank charges, they have to

enter data manually, every day, into their own ERP system or spreadsheets. They

have to reconcile this information with the data provided by each bank, each

with a different service level, reporting format, and reporting period. Some

banks send information via e-mail, others by fax or regular mail. Among other

things, the resulting inefficiencies hinder an organizations ability to make

decisions and comply with regulations.

Many of the top 20 global banks have undertaken

financial supply chain (FSC) initiatives to take a more active role in their

multinational clients’ trading activities, including collaboration with

logistics providers and import and export counterparties. Some have given

global product and sales responsibilities to their cash-management,

foreign-exchange and trade departments, standardizing systems, products, and

sales coverage. Others continue with regional trade product experts and

dedicated staff focused on specific customer segments.

Meanwhile, the Society for Worldwide

Interbank Financial Telecommunication (SWIFT), the

industry-owned co-operative that supplies messaging services and interface

software to thousands of financial institutions in hundreds of countries, has

completed its Trade Service Utility (TSU) pilot to provide standards, messaging

and matching engine for banks and is preparing to go live with global financial

institutions. The TSU project is designed to expand SWIFT’s focus from

traditional trade instruments to

supporting bank services across the entire corporate supply chain. TSU itself

does not enable corporations to connect to banks through a single application,

but it serves as a technical and standards foundation on which banks can build

their own applications for various financial supply-chain needs.

(c) SWIFT,

2006

Figure

1

Many banks are now in the process of building

proprietary applications with only limited multi-bank capabilities. For

example, a bank may prepare documents for export letters of credit and present

them to the confirming bank.

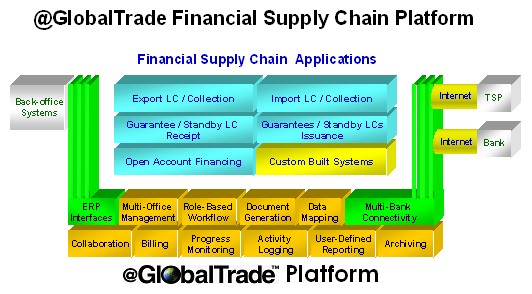

With a truly multi-bank platform, the corporate

client directs information electronically, in a standard format, to any bank in

its banking group, and receives information electronically, in a standard

format, from any bank in its bank group. Participation in such a platform is

not restricted by price or the need for special hardware or software. Access is

open and secure to meet banking standards.

The benefits of such a system affect many areas of an

organization. Finance and logistics staff preparing export letters of credit,

for example, can now prepare compliant documents while reducing errors that

could lead to discrepancies and late payments. The treasury department can

reduce Day Sales Outstanding (DSO) through collaborative electronic document preparation

and remote printing of documents at the bank. In addition, the treasurer and

CFO have access to real-time information on utilization of credit lines and

risk exposure to various countries and counterparties. While some of these

benefits such as DSO and cost savings can be quantified, others related to

visibility and real-time information are less tangible but equally important.

Figure 2

Our research has shown that corporates prefer to

purchase Application Service Provider (ASP) trade-service solutions from banks

rather than from software vendors for reasons involving business continuity and

compliance. Corporates regard banks as trusted third parties and see less risk

of business failure or data loss or theft when dealing with a financial institution.

They even prefer hosting a technology solution within a bank rather than

internally to reduce costs. The bank

can also offer a package deal of technology products and traditional trade

services. Meanwhile, the corporate client occupies the centre of the platform

and can improve communication not only with all its banks but also internally.

Figure 3

HypoVereinsbank, the third largest private bank in

Germany, introduced such a multi-bank platform, called GlobalTrade, last year,

as a multi-bank and multi-entity application that facilitates the uniform,

real-time, and secured exchange of information between all parties. HVB hosts

the platform for its customers and supports a full range of trade services as

well as agent services for guarantee facilities. In 2005, the European

Aeronautic Defense and Space Company (EADS), the world's second-largest

contractor for civil and military aircraft, with revenues of EUR 34.2 billion

in 2005, adopted the platform in connection with its EUR 2.9-billion Letter of

Guarantee (L/G) Umbrella Facility. HVB now acts as agent for EADS’s 36

subsidiaries and as service provider for the 22 banks participating in this

transaction.

Previously, each subsidiary managed its own L/G

activities. L/G exposure was spread over 47 banks, and 52 subsidiaries applied

independently for the issuance of L/Gs. Reconciliation of L/G data by EADS’s

head-office treasury was time-consuming and inefficient. Treasury monitored the

terms and the availability of L/G facilities and the allocation of business to

the banks.

In

adopting a multi-bank platform, EADS’s primary objectives were:

- to lock-in competitive terms & conditions for L/Gs for several

years;

- harmonization of documentation and saving of L/G commission;

- improved transparency and avoidance of discrepancies between banks'

and EADS's records;

- sustained flexibility for subsidiaries, but strong improvement of

efficiency and control;

- better diversification of business allocation between the banks,

and

- high acceptance of the new solution by subsidiaries and banks.

Since May 2006 EADS’s head office and subsidiaries

have used the platform to:

- standardize guarantee templates;

- submit electronically the L/G requests applied by EADS to the 22

banks;

- monitor the sub-limits for subsidiaries and banks;

- trace the status of each transaction;

- calculate the L/G fees, commitment fee, and the utilization fee,

and

- facilitate the request for indirect L/G fees from the banks.

All fees and commissions are settled by HVB on behalf

of EADS to the banks through a single consolidated fee account, and a system of

individually assigned reference numbers allows the automated allocation of fees

and commissions to each subsidiary through its inter-company account. The

platform provides tailor-made user administration and password handling for

EADS and the banks and automated file transfer to EADS' reporting systems.

Before accepting the solution, EADS subsidiaries

wanted reassurance about safeguarding operational and financial flexibility. To

this end, collaborative technology allowed the central treasury department to

intervene in the process only in cases that required exception processing. Meanwhile, consolidating the information

available from all banks in one web-based system reduced complexity and

considerably eased the task of monitoring and control for treasury and finance

personnel within subsidiaries and central treasury.

HVB and EADS’s guarantee platform project has proven

that multi-bank platforms can reduce costs and improve processes. It remains to

be seen how quickly true multi-bank platforms will be adopted in markets

outside Europe and by smaller organizations. Many banks are now going through

the challenge of positioning themselves in the landscape of financial

supply-chain services. They are looking for ways to differentiate themselves

from the competition, but most important they want to create additional revenue

streams. Doing this without the link to cheap credit is proving difficult.

Jacob Katsman is Chairman & CEO of GlobalTrade Corporation (www.globaltradecorp.com), a software developer and applications service provider, and Executive Director of the International Trade & Banking Institute (www.itbi.net).

SIDEBAR

BOTH SIDES NOW

The benefits of a multi-bank

trading platform affect banks and their customers, in different ways.

Corporate benefits from using a multi-bank platform

for processing guarantee and standby letter of credit transactions include:

- availability

of real-time information on utilization of credit lines across all banks –

no more searching through multiple, incompatible systems;

- fast

and accurate guarantee-application processing through the use of structured

workflows, electronic templates, standard clauses, and the ability to copy

from previous transactions;

- internal

savings from standardization of guarantee issuance across all business

divisions of a corporation and the treasury department;

- reduction

of errors through validation of key data fields in the application based

on pre- set approval levels;

- ability

to standardize and reduce commissions and commitment fees;

- ability

to monitor daily exchange-rate fluctuations and their effect on overall

credit availability;

- integration

with ERP systems for automated processing of large transaction volumes;

- simplified

verification and approval of bank charges;

- online

access to the guarantee application and the operative guarantees issued by

banks;

- easy

creation of reports answering such complex questions as: What guarantees

are outstanding with which bank? What is our credit-line utilization? What

charges have been paid to bank A in comparison with bank B, bank C, etc.?

- e-mail

alerts if a bank has not issued a guarantee or amended a guarantee within

the time specified in the service agreement.

The technology that facilitates these benefits could be purchased by the

corporate. Banks would then be invited to participate. Alternatively, a bank

could offer a hosted multi-bank solution to its clients.

For banks, a multi-bank platform presents the

following benefits:

- closer

long-term relationships with clients by becoming an integral part of

clients’ supply chain;

- additional

revenue through increasing the number of transactions as a result of the

closer relationship and service that the bank is providing;

- additional

transactional or license revenue as system provider and facilitator;

- ability

to offer value-added trade services, and

- capability

to easily offer outsourcing services, making use of the system’s

integration with clients’ supply chains.